In the second half of 2020, institutional investors increasingly started to show an interest in bitcoin. More and more investors have announced that they have allocated part of their cash reserves or a share of their fund toward bitcoin.

The most prominent one certainly has been Michael Saylor with his company MicroStrategy holding 70,470 bitcoin as of now. Another important development has been MassMutual Life Insurance Company converting a share of its fund into bitcoin. Particularly, the latter example has given much more legitimacy to bitcoin as an institutional investment asset. An insurance company that deems bitcoin safe enough to invest in is a game changer, as this industry is usually known for its very conservative investment strategies.

The inflow of institutional money appears to have become a self-reinforcing mechanism. Grayscales Bitcoin Trust alone has increased its bitcoin holdings by more than 66 percent from 365,090 on June 9, 2020 to 607,270 bitcoin on December 28, 2020, per bybt.com. In an appearance on CNBC’s “Squawk Box,” Michael Sonnenshein, Grayscale’s managing director, said that it sees inflows that are six-times that of last year on its platform and that the type of investors has changed. Some of the largest investors are now investing with Grayscale and these investors are holding bitcoin for the medium- to long-term.

While a domino effect for institutional investors can be observed, what is the underlining push for that? Why do these investors see the need to convert some of their capital to bitcoin? Saylor often talks about the need to convert a company’s cash reserves into bitcoin to protect its balance sheet against the dwindling value in fiat currencies, and particularly the U.S. dollar (USD) that has depreciated against other currencies over this year (as will be shown later in this article).

In a previous article, I have found that USD Google searches are strongly related to bitcoin searches and I have hypothesized that the impact of the dollar devaluation is more directly felt by people and that this leads to an increase in bitcoin purchase.

The USD has lost value against other major currencies in general. This can be seen in the USD index (DXY), which includes a basket of the following six exchange rates: EURUSD, USDJPY, GBPUSD, USDCAD, USDSEK and USDCHF.

One reason for that potentially is the unprecedented monetary expansion by the Federal Reserve Bank. However, not only the Fed expanded its balance sheet during this year — central banks like the European Central Bank (ECB) did as well, and other factors are at play too, which is why it makes sense to look at the DXY, which is affected by all of these factors. Changes in the world’s monetary landscape are an essential factor as well, as outlined in the excellent article “The Fraying of the US Global Currency Reserve System” by Lyn Alden. Due to this, it makes sense to look at the DXY development vis-á-vis the bitcoin price.

Before looking at the USD index relationship with bitcoin’s price, let us first examine the Fed balance sheet and the bitcoin price. This relationship is shown in Figure 1.

The bitcoin price and the size of the Fed balance sheet seem to be somewhat related. However, the price does not directly follow the balance sheet expansion during the first half of the year.

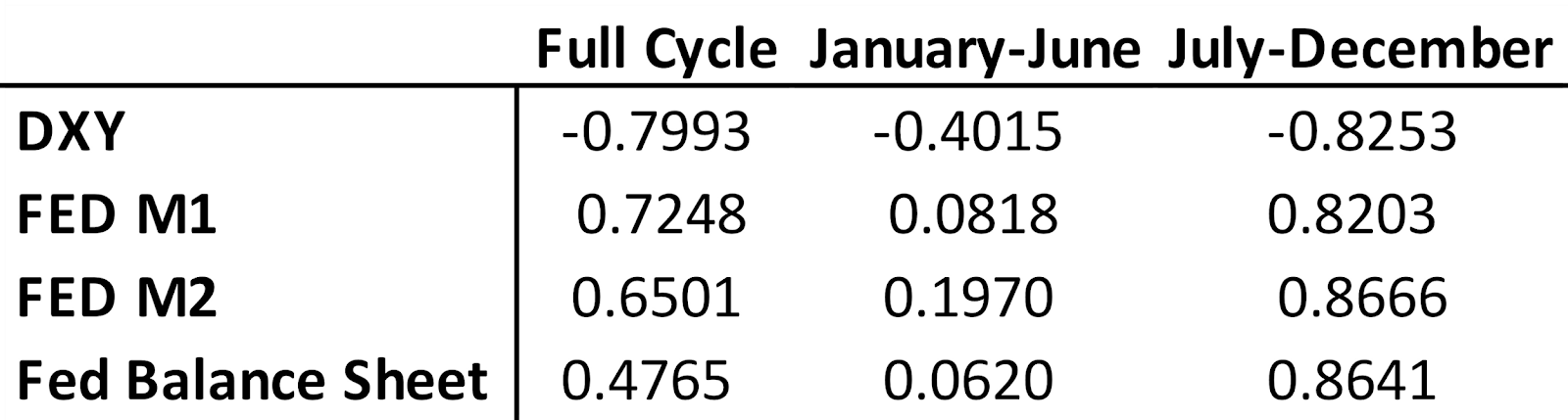

This can also be seen in the correlation coefficients in Table 1. Over the whole period, both variables are correlated by 47.65 percent, whereas in the first half of the year it is only 6.20 percent and has strongly increased in the second half of the year to 86.41 percent. A very similar picture emerges for the money stock M1 and M2 over this year.

While M1 has increased by over 65 percent, M2 increased by nearly 26 percent. The relationship of the monetary variables and bitcoin price seems to exist but does not appear to be as strong as for the DXY.

Over the whole year, the value of the DXY shows a strong negative relationship with the bitcoin price (see Table 1). It is much higher compared to the other two variables. This makes sense if we consider the fact that the U.S. dollar has not only lost value against other currencies due to monetary policy but also due to other mechanics at play. That is why the USD’s dwindling value against other currencies seems to be the more relevant variable.

Looking at Figure 2, the DXY tracks the bitcoin price surprisingly well. This seems to mainly be true during the second half of the year after the DXY did break below 95 on July 22, 2020. This also seems to coincide with a rise in institutional interest in July and August. Interestingly, the DXY appears to be positively related with the bitcoin price during the first half of the year where the DXY has been predominantly ranging between 95 and 100.

Looking at the correlation, however, it was already negative in the first half of the year (-0.4015). This only grew stronger in the second half, with a coefficient of -0.8253. While the dollar value had not been that important in the first half of the year, the breakdown in value seemed to have pushed investors over the edge and, with that, increased its relevance for the bitcoin price.

While the above relationships are only correlations, the relationship nevertheless seems to be strong and, as a narrative, it seems to be an essential driver of institutional interest. Irrespective of what you think about which of these variables is effectively pushing institutions into bitcoin, monetary policy and the dwindling value of fiat currencies seems to be at the forefront of it.

By the looks of it, the loose monetary conditions are here to stay and, as Alden explains in the aforementioned article, the trend of the declining value of the USD relative to other currencies will likely continue in the future. With USD’s bearish outlook against other currencies, the devaluation of currencies against hard assets, unprecedented monetary intervention that seems to be here to stay and the domino effect at play, expect more and more institutional investors to FOMO into bitcoin in 2021. All in all, this is bullish for bitcoin.

This is a guest post by Jan Wuestenfeld. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

The post How Monetary Policy And Dollar Devaluation Are Driving Institutional Interest In Bitcoin appeared first on Bitcoin Magazine.

Leave a Reply